LBRG Just Became A Tier 1 Supplier To A $700 Billion Industry

- Checkers

- Jun 15

- 4 min read

The EV supply chain is being rebuilt around automation and AI, and the equipment makers one layer beneath the automakers are turning into some of the most valuable companies in manufacturing. Ladybug Resource Group, Inc. (OTCID: $LBRG) just bought its way into that layer, acquiring Guangzhou JingDiao Automotive Equipment Manufacturing in April and becoming a Tier 1 and Tier 2 supplier to globally recognized automotive brands in South China's equipment corridor. The operation comes with partnerships already in place, among them Mino, the integrator whose body-shop lines run inside Mercedes-Benz, BMW, and Ford plants.

The arena it just stepped into is enormous and growing fast. MarketsandMarkets projects the global EV market to expand from $699 billion in 2025 to $1.19 trillion by 2035, with the equipment layer that actually builds the vehicles, the machinery LBRG now owns, growing from roughly $32 billion in 2025 to $42 billion by 2030. The automation on top of it climbs faster still, with AI in manufacturing projected to grow from $34 billion in 2025 to $155 billion by 2030, a 35% compound rate among the steepest in any industrial market. That spending flows fastest to the suppliers that can do the most of the job themselves, without farming the hard steps out.

LBRG's floor takes a drawing in at one end and turns out a finished, coated part at the other, running it through integrated design, 5-axis CNC machining, a laser cutting line nearly sixty feet long, and a certified paint shop without ever handing it to a subcontractor. Most suppliers own one of those stations and rent the rest, machining a part and shipping it out to be cut, or cutting it and shipping it out to be painted, and every time a part leaves the building it takes a week and a margin with it. The shop that can quote the whole sequence is the one that wins the program, and the EV transition is filling order books with exactly that kind of work, the aluminum battery trays and high-strength chassis members that have to be cut, formed, and finished to tolerance in a single pass. Running a floor that does all of it at once, in sync, is a harder problem than buying the machines that do it.

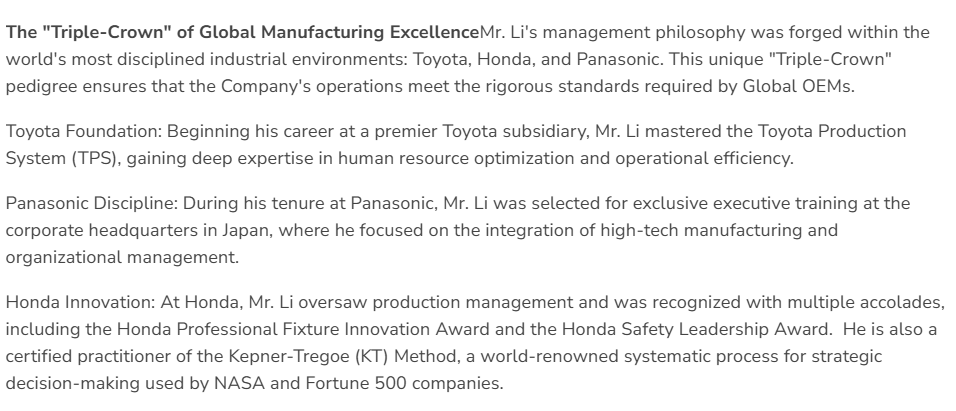

That problem is what Shicai Li spent a career learning to solve. Now head of LBRG's manufacturing operation, Li put in close to twenty years inside Toyota, Honda, and Panasonic, where he learned the Toyota Production System from the company that invented it, the just-in-time, build-the-quality-in discipline that made Toyota the most efficient manufacturer on earth. When he founded the company in 2016 he wrote that discipline into software, a manufacturing execution system that tracks every job from the 3D model to final inspection and reads each machine on the floor as it runs. Because LBRG owns the code outright instead of licensing it, the idle minutes the system strips out of the schedule fall to the company's own margin rather than a vendor's invoice.

The scheduling now runs tight enough that the laser and CNC lines take on more EV work without another machine or another shift, and LBRG has reported the result in its margins, record EBITDA and shorter lead times. The same job-level data hands it an unusual lever over its supplier relationships, letting it settle with secondary fabricators in thirty days while most of the industry stretches them to ninety, the kind of term that quietly pulls the better shops onto its programs. It has since added an AI layer to the line, vision models that check parts as they are made and pull a defect before it reaches the next station instead of after the batch is finished, and the same inspection units sold into the packaging industry have run gross margins near 57%. A rival with enough capital could, given time, assemble most of that, but the paint shop is the one piece it could not.

The reason is that the paint shop runs on permits a competitor can no longer get. LBRG's painting and surface-treatment lines passed the 2026 environmental audits and hold a full certification to operate, and the worth of that approval lies in what is happening around it. China's GB 30981 coatings standard took effect this year, the VOC permit regimes in Shanghai and Beijing keep tightening, and new permits for industrial painting and chemical surface treatment have all but stopped being issued where this work is done. Demand is moving the other way, as Tesla- and BMW-class automakers run net-zero supplier mandates that shut uncertified shops out of new programs, so the certified line sits on the right side of both walls, holding an approval rivals cannot obtain and customers increasingly require, and the company puts the operating payoff at a thirty percent lower logistics carbon footprint and a fifth off its lead times.

While LBRG sits at a $1.6 million market cap, the companies that handle a single piece of what it does are valued in the billions. Cognex (NASDAQ: $CGNX) is worth around $10.6 billion for machine-vision inspection alone. Han's Laser is worth around $9 billion on $2.7 billion in revenue for laser systems that are close cousins to the ones on LBRG's floor. Rockwell Automation (NYSE: $ROK) commands near 5.5x revenue for the kind of factory software LBRG owns outright, and Dürr built a multibillion-dollar business largely on the automotive paint lines LBRG now runs certified. Each commands billions for one of the capabilities LBRG now runs together, with a market cap less than the cost of a single machine on its floor.

Disclaimer: Mt. Zion Market Ventures has received compensation for the creation and dissemination of this article. For more information, please visit opendisclose.com. The information provided here is not intended to be a comprehensive analysis of the subjects mentioned. All information, opinions, and forecasts contained herein should not be construed as investment advice, a recommendation, or an offer to buy or sell any securities or related financial instruments. Investors should conduct their own research or consult with a qualified financial advisor before making any investment decisions. The author and publisher of this content are not responsible for any losses, damages, or other consequences that may result from the use of the information provided. Investing in stocks, including those mentioned here, involves risks, including the risk of loss.